Finding houses to flip can be difficult, but that doesn’t mean that you should jump at the first opportunity you come across. A rehabber also needs to know how to choose the right property. In this section, we explain how to choose houses to flip by looking at location, physical characteristics, financial considerations, and more.

Location

You’ve heard it before, and it’s true — location, location, location.

You’ve heard it before, and it’s true — location, location, location.

Nothing will determine the value of your house flip more than where it is located, starting with the city, and further consideration given to neighborhood, location within a neighborhood (busy street, quiet street, etc.), school district, and even school.

Proximity to positive factors such as stores and public transportation will increase value, while proximity to negative factors, such as highways and airports will decrease value.

When looking to choose a house to flip, you need to understand the property in the context of where it sits. To figure this out, you need to start with who you expect the purchaser to be.

- Is the neighborhood full of young, single people? If so, the school district becomes less important.

- Is the purchaser a young couple with small children? Then, the school district becomes highly important.

- Is the environment urban, where owning a car is a luxury? If so, then you need to consider the proximity of your property to public transportation.

- Is the area missing easy access to public transportation? Then you should find a house with parking included.

- Does your neighborhood have ample parking? Does the property have a driveway or garage?

There are many questions like this that need to be understood before committing to a rehab project.

Do the same research that your buyers will do. Utilize websites to familiarize yourself with your area. Different towns and counties, can have dramatically different tax rates for school taxes and real estate taxes. Some townships may pick up trash twice as a municipal service. Others do not pick up trash at all and you will have to enter into a private contract for trash removal. You should know these things about your property.

If the quality of schools is an issue, research lists of the best schools in the area you are interested in working with. Look at the websites of school districts to see what kind of budget they have, what their expenditures per student are and what awards they have been given. You can be sure that the top school districts will let you know about their accomplishments on the website.

Know your customer and apply that knowledge to all aspects of your property’s location. By doing so, you can tailor your project to meet their needs and help make your project successful.

Physical Characteristics of The Rehab Property

Physical Characteristics of The Rehab Property

Physical Characteristics of The Rehab Property

Physical Characteristics of The Rehab PropertyWhile you want your property to be different in some ways from other properties for sale in the area, you want it to fundamentally conform, or be better than the local competition for sale.

For example, if all of the homes in the neighborhood are 1,800 square foot, three bedroom, two bath homes, you may have trouble selling a home that is 1,500 square feet, two bedrooms and one bath, unless you are willing to make a considerable financial concession. You will want your house flip project in this neighborhood to be at least 1,700 square feet, three bedrooms and two baths.

Don’t over do it, though! A property with more than 2,100 square feet, four bedrooms and two baths, could be too expensive for that neighborhood. Your project should conform to the neighborhood in square footage, but be different in other ways through your choice of finishes, landscaping and overall curb appeal.

Larger than average lots in the neighborhood are generally favored. Be prepared for a price adjustment if the lot is smaller than average. Make the most of what you have. Providing privacy for the yard through fencing or landscaping, and making the yard appealing can make a significant difference in your house flip.

Use your imagination when picking a house to flip. Frequently, the most successful projects are the ones that need the most work. If the condition is poor, see if there is a similar nearby house for sale that’s in better condition. Tour the other house for sale to better visualize what is possible in the house you are looking at. Don’t let the poor condition deter you, as long as most of the fixes are cosmetic.

If you suspect structural issues, however, be very careful. Unless you have significant rehab experience, remediation of structural problems can be extremely difficult and costly.

When evaluating whether to buy a property for house flipping purposes, you need to understand what will make your property more interesting than other similar properties for sale in the neighborhood. For the end owner, buying a home can be an extremely emotional decision. You need to figure out what will make someone fall in love with the property. Although high end finishes on the inside are very important, you want to grab the customer at the street, so pay very careful attention to the overall exterior condition and curb appeal of the property.

Do the same research that your buyers will do so you can tailor your project to meet their needs.

Financial Considerations

Financial Considerations

Financial ConsiderationsIf you want to know how to choose a house to flip, there’s no way around it- you have to know how to look at the numbers. The financial considerations relevant to your property investment depend on whether you’re renting or flipping a property, and we’ll discuss both scenarios here.

Rental Properties

Some investors decide to rehab a property for the purpose of renting it. Here’s how you can evaluate the financials of these types of investments.

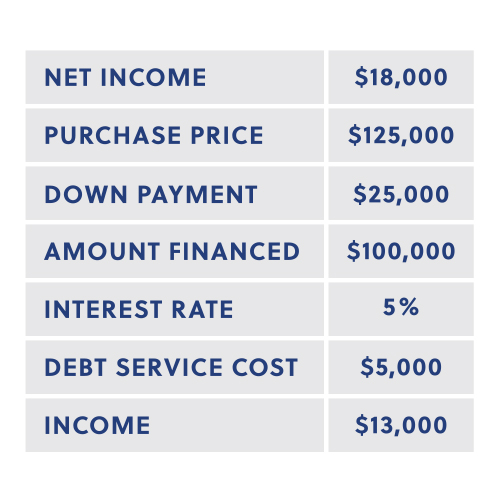

Example Scenario:

The following section details a number of financial equations that can be useful in the decision making process. For the purposes of consistency, all the following equations will use the following figures:

The Cap Rate (Capitalization Rate) is a methodology for figuring out the value of an income property. It is derived by dividing the annual Net Operating Income (NOI) by the purchase price. The resulting number is the Cap Rate. For example, assume that a property is priced at $125,000, and its NOI is $14,000. The cap rate would be 11.2%.

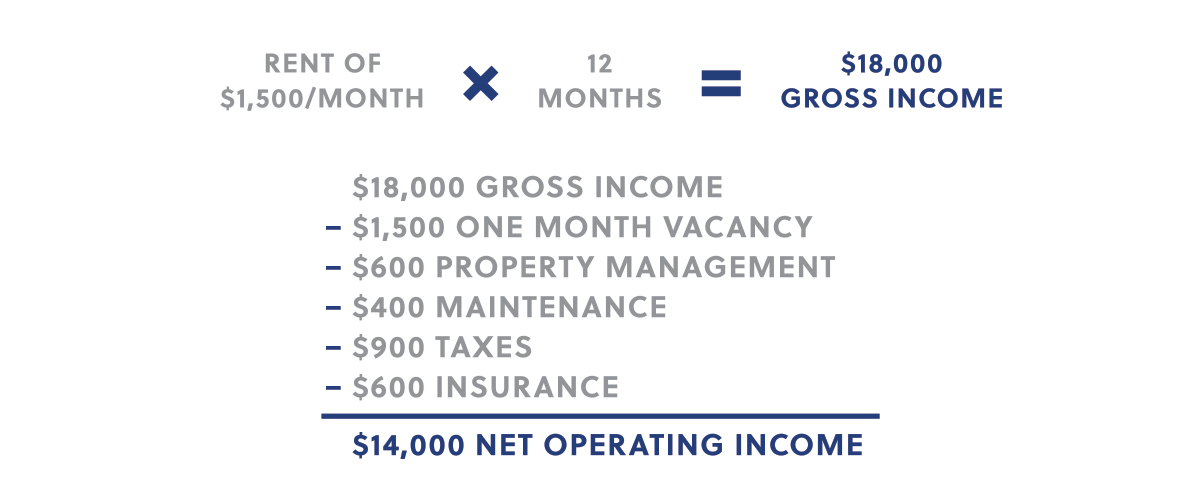

It is easy to determine the sales price of a property, but how do you determine NOI? NOI is calculated by taking the projected gross income from rent on the property (with an allowance for vacancy) and deducting all of the costs associated with that property, including, but not limited to taxes, insurance and maintenance. Only after all of the potential expenses and vacancies are accounted for can a true NOI be derived.

It is easy to determine the sales price of a property, but how do you determine NOI? NOI is calculated by taking the projected gross income from rent on the property (with an allowance for vacancy) and deducting all of the costs associated with that property, including, but not limited to taxes, insurance and maintenance. Only after all of the potential expenses and vacancies are accounted for can a true NOI be derived.

OK, now that you understand how to obtain a cap rate, what does it mean?

OK, now that you understand how to obtain a cap rate, what does it mean?

It’s a starting place for evaluating market value, if not the profitability of a given deal. It provides a tool for investors to use for roughly valuing a property based on its NOI. A comparatively lower cap rate for a property would indicate less risk associated with the investment (increasing demand for the product), and a comparatively higher cap rate for a property might indicate more risk (reduced demand for the product).

However, cap rates don’t really indicate what the return will be, unless the borrower is paying all cash. It assumes that the income and expense numbers are accurate. Accordingly, when someone is trying to convince you to purchase a property by throwing cap rates out, remember that cap rates are not the best measure for a property that is financed.

If financing the purchase, the price and net cash flow are both used to determine a cap rate, and then that rate is compared to the market cap of similar properties in the area. In this case the cap rate is determined by dividing your property’s annual net cash flow (without deducting your mortgage payments) by your total purchase price. This is used to evaluate the property income only and does not take into consideration how you might choose to finance your acquisition.

Your “pre-tax cash on cash return” on the other hand, does take your financing into consideration. In this equation, you divide the net annual cash flow from the property (after deducting your debt-service payments) by your cash down payment to acquire the property (not the total purchase price).

Your “pre-tax cash on cash return” on the other hand, does take your financing into consideration. In this equation, you divide the net annual cash flow from the property (after deducting your debt-service payments) by your cash down payment to acquire the property (not the total purchase price).

In the end, make sure that you understand the analysis and that you are comparing apples to apples. Comparing the cap rate of a property that is a financed to a property that was paid for in cash, is like comparing apples to oranges – it is simply not the same thing.

In the end, make sure that you understand the analysis and that you are comparing apples to apples. Comparing the cap rate of a property that is a financed to a property that was paid for in cash, is like comparing apples to oranges – it is simply not the same thing.

Property Flip

Other investors choose to rehab a house for the purpose of a quick sale. Here’s how to calculate the financials for those scenarios.

Economic measurements such as cap rate and cash flow are not relevant when looking at a house flip. Instead of a stream of income over an extended amount of time, you must look for income at a single point when the property is sold. The fundamental analysis that needs to be done for a house flip is how much is it going to cost you versus how much are you going to sell it for.

The analysis required is not as easy as it seems, as almost all of the contributing numbers will be speculative. The only thing you will know at the beginning of the project is how much you will pay for it and the associated closing costs. Everything else will be speculation. You can make an educated estimate regarding how much the rehab work will cost, but there is rarely a rehab project without an unexpected expense.

You can think that the project will take six months, and budget accordingly, but if it takes longer, everything costs more. For example, you will need to pay taxes, utilities and insurance for the additional amounts of time, the cost of the financing of the project will continue to accrue each day that the loan goes unpaid.

Lastly, the best you can do to estimate the selling price at the end of the project is to do your homework, but be mindful that houses within a particular neighborhood sell within a range of prices. Rarely do similar homes sell for the exact same amount. Be aware that seasonality can affect home prices and certain times of year are harder months to sell homes in. Typically, prices are highest and homes sell most frequently in the late spring and early summer months while prices are lowest and marketing times are highest in the winter.

Control your costs, do your homework, project conservatively, and finish your rehab in a timely manner, and you are likely to have a successful flip project.

If your lender is telling you there is not enough equity in the rehab project, believe them!

Follow the Rules

Follow the Rules

Follow the RulesTypically, most rehab lenders will lend between 65 and 70% of ARV (after repaired value). There is a very good reason for that. A house flipper is generally borrowing money on an investment property, with the expectation of making money from the project. If the cost of the property plus rehab exceeds 65 or 70% of the ARV, it is possible that there will not be enough equity in the deal for the investor to make money in the end.

It is important not to forget that in addition to the purchase and rehab, there are closing costs, carrying costs (including, but not limited to, taxes, insurance, mortgage payments and utilities) that will eat into the equity on a daily basis.

Also, remember that properties are not sold for free. When selling the rehab project, you will likely have to pay a real estate agent, transfer taxes, recording fees, etc. Buying, financing and selling a property can add up to 20% to the cost of the project, in addition to the purchase and rehab costs, reducing the 65-70% cost to ARV, to 85-90%, leaving little profit for the flipper.

Follow the advice! Lenders only make money when they make a loan. If your lender is telling you there is not enough equity in the project, believe them! You can always find other properties and choose a better house to flip.